17.07.24

17.07.24

Österreichs Sparquote: Wird weniger gespart oder sinken nur die Zinsen? (Martin Ertl)

05 Nov

Die Sparquote sinkt, allerdings nicht nur deswegen, weil weniger gespart wird. 40 % der Finanzvermögen der Haushalte werden auf Bankeinlagen veranlagt. Der Rückgang der Sparquote hängt stark mit dem Rückgang der Sparzinsen zusammen. Private Finanzvorsorge gewinnt angesichts niedriger Zinsen und den Sorgen um die langfristige finanzielle Nachhaltigkeit des öffentlichen Pensionssystems an Bedeutung. Allerdings beobachtet man in Österreich seit 2008 einen starken Rückgang der Sparquote. Die Sparquote, welche sich als Differenz aus den verfügbaren Einkommen der privaten Haushalte und den Konsumausgaben errechnet, fiel seit ihrem Höchststand von 13,0 % in 2008 auf 6,6 % im zweiten Quartal 2018 (Grafik 1). Der Rückgang der Einkommen im Zuge der Fina... » Weiterlesen

ECB affirms its monetary policy outlook & Buoyant U.S. growth continues (Martin Ertl)

29 Oct

The ECB Governing Council sees no need to change its monetary policy and economic outlook. Recent data have been “somewhat weaker than expected” but remain broadly in line. Core inflation is expected to pick-up in Q4 and to be supported by accelerating wage growth over the medium-term. Economic growth is expected to remain close to the current pace over the medium-term with slight downside potential in Q3. Euro Area sentiment continues its decline, though still remaining in expansionary territory. The ECB has kept interest rates unchanged at last week’s monetary policy meeting of the ECB Governing Council. The ECB’s key monetary policy interest rate remains at 0 % and the marginal and the deposit facility interest rates are kept at 0.25 % and -0.4 %. This is well in ... » Weiterlesen

Economic Convergence in Central and Eastern Europe revisited (Martin Ertl)

23 Oct

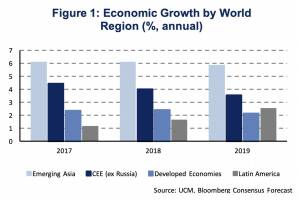

CEE economies are closing the income gap to Western Europe. Convergence was strongest in the immediate pre-crisis period and has diminished since then, though, remains active at least within the EU. Convergence has been faster within the EU than in non-EU countries and particularly rapid in EU member states of the CEE region. Education and FDI are positively associated with GDP per capita growth, as is institutional quality within the EU. Central and Eastern Europe (CEE) is among the fastest growing world regions. In 2017, gross domestic product (GDP) in CEE, excluding Russia, expanded by 4.4 %[1]. Only Emerging Asia was growing more rapidly (6.1 %) while Developed Economies (2.4 %) and Latin America (1.1 %) experienced slower growth, as did the global economy (3.7 %). Moreover, strong gro... » Weiterlesen

Italy’s public debt sustainability 2.0: the effects of a new fiscal outlook (Marti...

19 Oct

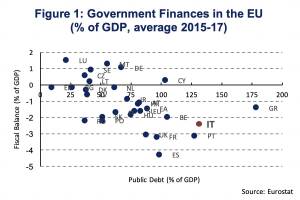

Italy has among the highest public debt levels within the EU, only topped by Greece. Yet, the ruling coalition plans to raise the fiscal deficit, questioning public debt sustainability. The new fiscal outlook leads to a substantial deviation from the previous trajectory of public debt normalization, yet is not as excessive to make public debt unsustainable. Public debt to GDP will decrease only very gradually over the medium-term which does not comply with EU regulations and, if not adjusted, may results in an excessive deficit procedure. The Italian ruling coalition, between the League and the Five Star Movement, announced its medium-term budget plan. The general government deficit was set at 2.4 % of GDP for the year 2019. This is significantly above the previous government’s deficit... » Weiterlesen

Quarterly Macroeconomic Outlook: Economic growth slows down but fundamentals remai...

10 Oct

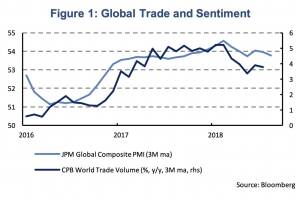

The global economy continues to expand solidly with the business cycle accelerating in the United States and slowing down in the Euro Area as well as some emerging market economies. The economic outlook of the Central Eastern European region remains favorable, despite of emerging market turbulences. We project growth at 4.0 % (2018) and 3.5 % (2019) for CEE (ex Russia). The global economy continues to grow at a solid pace, the peak has, however, most likely been reached and downside risks related to trade protectionism have intensified. The September 2018 economic outlook by the OECD projects world GDP to grow at 3.7 % in 2018 and 2019. The growth rate in the volume of world trade has decelerated during the last 4 quarters from 5.2 % in Q3 2017 to 3.9 % in Q2 2018. Global economic sentiment, tho... » Weiterlesen

31.07.24

31.07.24

global market. 7 Monate 2024 sind vorbei und die Wiener Börse hat in diesen sieben Monaten mehr Handelsvolumina verbuchen können als in den ersten 7 Monaten 2023, der Zuwachs ist im einstelligen Prozentbereich, aber immerhin. Auch im früher stark promoteten global market ist es erstmals seit Jahren wieder etwas nach oben gegangen, im Gesamtjahr 2021 lag dort das Jahresvolumen noch bei 5,5 Mrd. (das ist ca. ein Monatsumsatz im Prime Market), 2022 waren es nur noch 1,3 Mrd.. und 2023 gab es sogar den Fall unter die Mrd. Euro. In den ersten sieben Monaten 2024 ist es wieder leicht nach oben gegangen, ob die Mrd. End of Year wieder erreicht werden kann, ist aber unklar. Es gibt zwar im global market günstige Konditionen, aber die Broker stellen Wien bei den internationalen Aktien nicht so in die Pole Position und die Markttiefe könnte natürlich ebenfalls besser sein. Keine einfache Aufgabe, diese wichtigste Aktienfacette im Vienna MTF, denn es geht immerhin um die wichtigsten Aktien der Welt. Ich bin ja der Meinung, dass das Tagesgeschäft viel mehr promotet gehört, davon würde auch der global market profitieren.