No signs of abrupt growth slowdown in CEE (Martin Ertl)

Czech Republic, Hungary, Slovakia and Poland

- Growth momentum in Central Europe remains strong during the third quarter, even accelerating in Poland.

- In Hungary and Slovakia growth momentum remains elevated with inflationary pressures building up gradually.

- While core inflation has moved beyond 2 % in Hungary and Slovakia it remains subdued in Poland at below 1 %.

- Growth has slowed down in the Czech Republic compared to strong growth in 2017. Capacity constraints are intensifying as firms face the tightest labor market in the region.

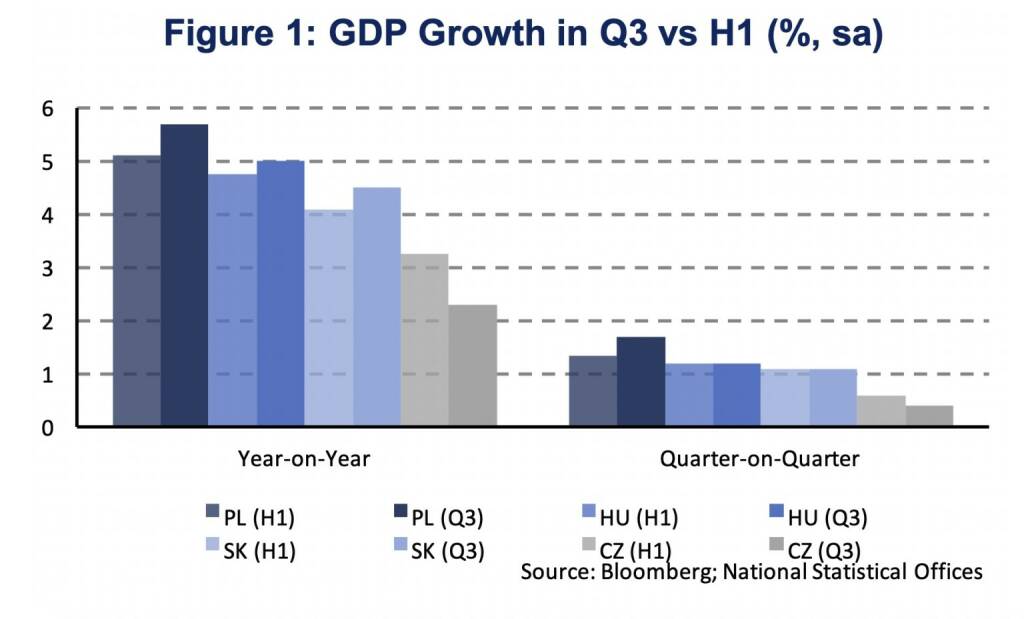

During the third quarter (Q3) economic growth in Central Europe (CE) was stronger than expected in all CE economies except for the Czech Republic (CZ). Economic growth was strongest in Poland (PL) at 5.7 %, seasonally adjusted (sa), compared to Q3 2017 (y/y). Growth momentum in Poland accelerated compared to the first half of the year (H1), as shown by a rise in quarter-on-quarter (q/q) GDP growth (Figure 1). In Hungary and Slovakia growth momentum remained elevated but hasn’t expanded any further in Q3. In both economies q/q growth remained constant above 1 % in Q3 compared to H1 2018 (HU: 1.2 %; SK: 1.1 %). Seasonally adjusted year-on-year growth increased to 5.0 % in Hungary and 4.5 % in Slovakia. In the Czech Republic growth momentum has declined to 0.4 % seasonally adjusted quarter-on-quarter growth compared to 0.6 % in H1. Year-on-year growth has declined sharply to 2.3 % (H1: 3.3 %), which is also due to strong growth in H1 2017 averaging 1.9 % (q/q).

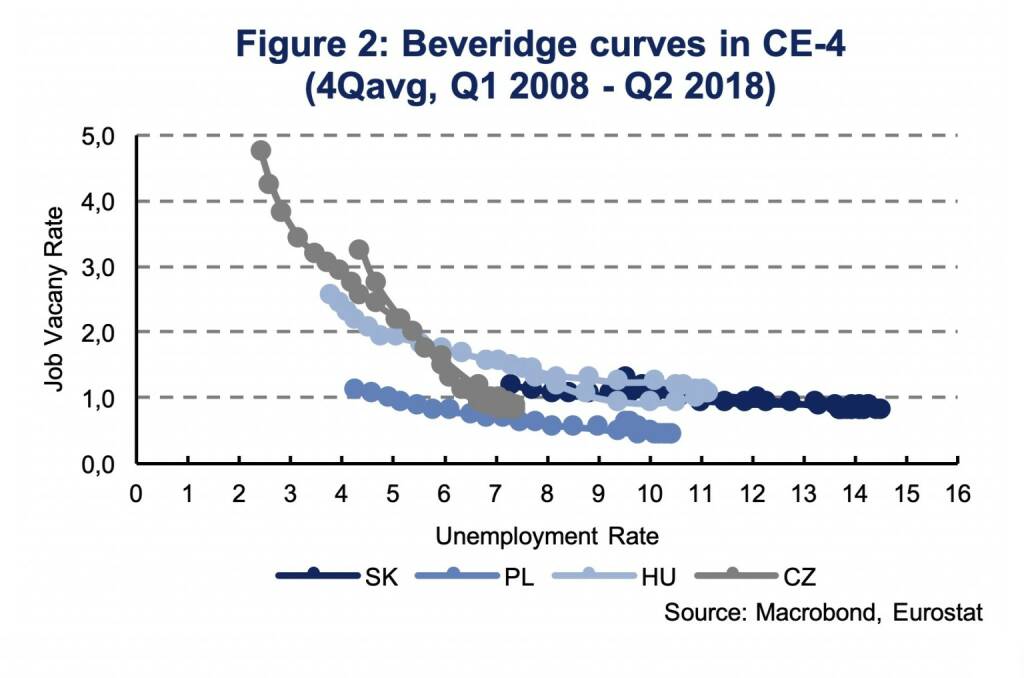

During the first half of the year GDP growth has mainly been driven by domestic demand. Household consumption and investment activity contributed positively to GDP growth while net exports (exports minus imports), except for Slovakia, have dampened growth moderately. So far, only the headline figures for GDP growth have been released for the third quarter with no information about the composition of growth. Nevertheless, it is fair to assume domestic demand to have played the dominant role also during the third quarter. Private consumption should continue to be driven by historically tight labor markets with unemployment rates at 2.3 % in the Czech Republic, 3.7 % in Hungary and Poland, and 6.9 % in Slovakia (Q3). Relating unemployment rates to job vacancy rates gives a good indication of labor market tightness, also known as Beveridge curves (Figure 2). Using this metric identifies the Czech Republic as having the tightest labor market among CE-4 economies, with the lowest unemployment rate and the highest job vacancy rate (Q2: 5.4 %) [1]. In Hungary, already 2.7 % of labor demand (number of occupied posts plus number of job vacancies) are vacant. In Poland and Slovakia job vacancy rates are less pronounced (1.2 %). The marked difference in unemployment rates between Poland and Slovakia, at similar job vacancy rates, shows how structurally efficient/inefficient the Polish/Slovak labor market is.

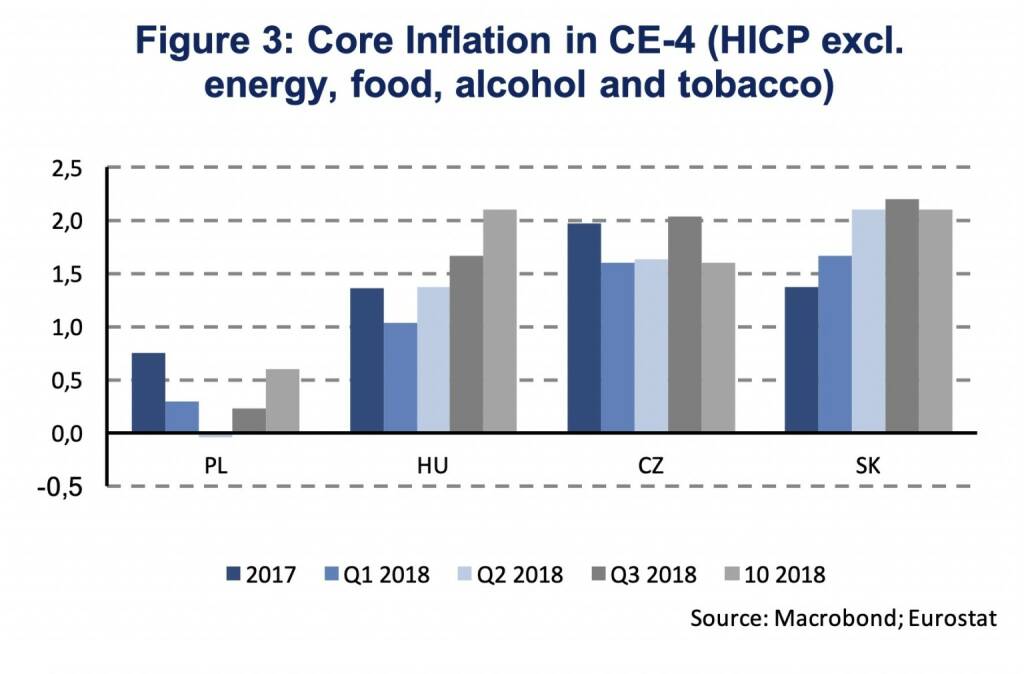

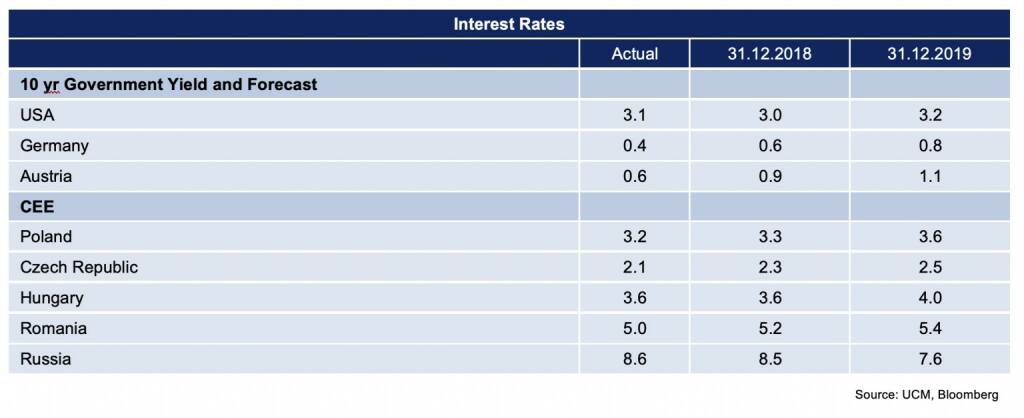

With unemployment rates at historic lows and economic growth above its long-term potential, domestic prices pressure should be building up. Evidence on inflation to rise is, indeed, getting more consistent lately, arriving with a considerable time lag. Inflationary dynamics of the domestic economy are usually measured by looking at core inflation rates, which exclude volatile prices of energy, food, alcohol and tobacco. Core inflation has been rising throughout the year in Hungary and Slovakia, reaching 2.1 % in October (Figure 3). In the Czech Republic inflation has already increased more markedly in 2017, while remaining rather consistently below 2 % in 2018. In fighting inflation to stay beyond 2 % over the medium term, the Czech National Bank (CNB) has increased monetary policy interest rates 4 times this year. Poland is the only Central European economy where inflation has remained subdued. Core inflation has only recently started to accelerate somewhat but has not yet moved beyond 2017 levels. Thus, it does not come as a surprise that monetary policy differs substantially between the Czech Republic and Poland. The National Bank of Poland (NBP) has signaled to keep monetary policy unchanged, at least, until the end of 2019. In Hungary, where the inflation target is at 3 % (PL: 2.5 %, CZ: 2 %), the National Bank of Hungary (NBH) has, so far, maintained a loose monetary policy. With core inflation rising and inflation likely to surpass the central bank’s forecast in Q4 2018, the NBH may have to commit to its forward guidance rather sooner than later. The NBH has only recently added a sentence on monetary policy normalization to its statement in September: “the Council is prepared for the gradual and cautious normalization of monetary policy, which will start depending on the outlook for inflation” [2]. The Monetary Council of the NBH already meets this week (20th of November). The next inflation projection will, however, only be released in December.

Russia and Ukraine

- While the macroeconomic picture remains positive, early signals suggest a growth slowdown until year-end in Russia.

- Ukraine continues its economic recovery.

In Q3, Russia’s GDP expanded by 1.3 % (y/y) after rising by 1.9 % in the previous quarter. In our own seasonally-adjusted calculation, this is equivalent to a quarter-over-quarter decline by 0.3 %. The weak quarterly GDP outcome poses downside risks to our forecast on 1.9 % GDP growth in the total of 2018 (Bloomberg consensus: 1.8 %). There is no expenditure breakdown available yet. In Q2, household consumption (+2.6 % y/y), fixed investment (+1.0 %) and exports (+7.3 %) as well as imports (+2.8 %) were expanding.

Both real and nominal wage growth had peaked early in the year (10.1 % and 12.5 % y/y in February) and slowed afterwards (7.2 % and 10.4 % in September). At the same time, the inflation rate rose to 3.5 % in October (from a low at 2.2 % in January/February). Monthly retail and car sales slowed equivalently until September/October (2.2 % and 8.3 %). Car sales exhibited double digit growth rates earlier in the year and in 2017. On the other side, rising bank lending to households (22.0 % y/y) keeps supporting private expenditure. After a sharp drop in 2015/16, household lending made a strong recovery. While the macroeconomic development remains broadly stable, recent evidence suggest a short-term growth slowdown towards year-end.

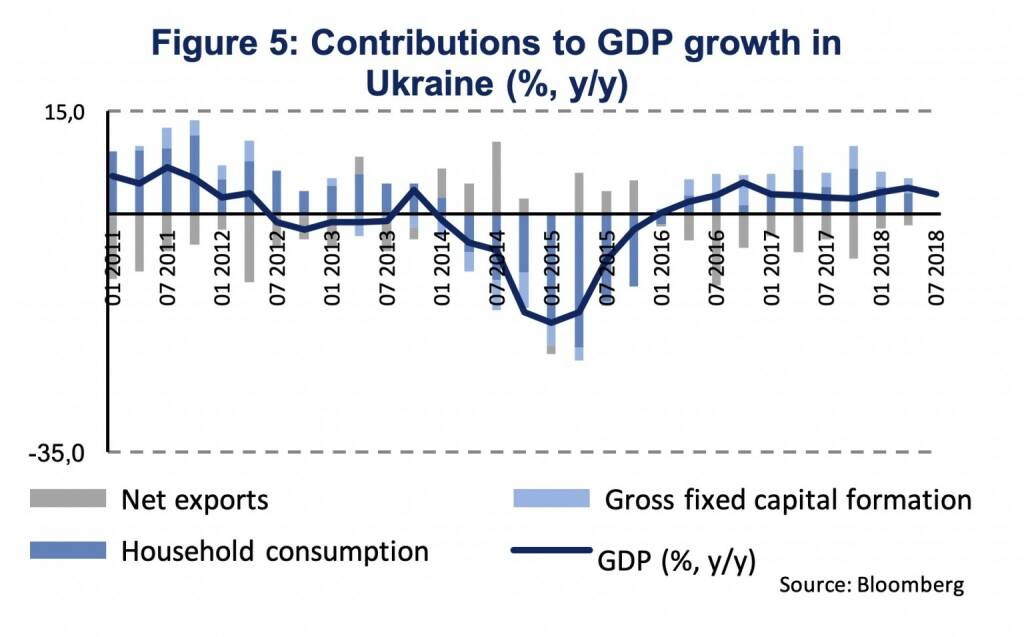

The Ukraine economy grew by 2.8 % (y/y) in Q3 after growth of 3.5 % during the first half of 2018. During H1, economic growth was strongly expelled by private consumption and gross fixed capital formation (+4.9 % and +15.6 % y/y), while net exports were a drag on growth (Figure 5). Agriculture (+19.3 %), manufacturing (+2.0 %), wholesale and retail trade (+3.8 %) and the energy sector (+6.9 %) contributed strongly to economic growth in Q2. GDP growth in Q3 was broadly in line with our forecast of 3.0 % growth during the whole year.

In September, retails sales rose by 5.5 % (y/y), while retail sales growth averaged 6.8 % since the beginning of the year. Household consumption remains supported by elevated growth in wages & salaries. Total real monthly wages rose by 14.1 % (y/y) in October and by 14.3 % since January. Overall, short-term data also suggest a continuation of the economic recovery.

[1] The job vacancy rate is defined as the number of job vacancies as a share of the number of occupied posts plus the number of job vacancies.

[2] The NBH’s Monetary Council statements can be found here: https://www.mnb.hu/en/monetary-policy/the-monetary-council/press-releases (accessed: 16th of November 2018).

Authors

Martin Ertl Franz Xaver Zobl

Chief Economist Economist

UNIQA Capital Markets GmbH UNIQA Capital Markets GmbH

Latest Blogs

» SportWoche Podcast #124: Liam Ferguson, de...

» Österreich-Depots: Ultimo-Bilanz mit Addik...

» Börsegeschichte 30.8.: Warren Buffett (Bör...

» PIR-News: Zahlen von Warimpex, Strabag, Ne...

» Nachlese: Karin Bauer, LLB Aktien Österrei...

» Wiener Börse Party #727: Nächster Rekord-T...

» Börsenradio Live-Blick 30/8: DAX krönt Erh...

» Börse-Inputs auf Spotify zu u.a. ATX TR, L...

» ATX-Trends: Immofinanz, UBM, CA Immo, S Im...

» Börsepeople im Podcast S14/17: Karin Bauer

Weitere Blogs von Martin Ertl

» Stabilization at a moderate pace (Martin E...

Business and sentiment indicators have stabilized at low levels, a turning point has not yet b...

» USA: The ‘Mid-cycle’ adjustment in key int...

US: The ‘Mid-cycle’ interest rate adjustment is done. The Fed concludes its adj...

» Quarterly Macroeconomic Outlook: Lower gro...

Global economic prospects further weakened as trade disputes remain unsolved. Deceleration has...

» Macroeconomic effects of unconventional mo...

New monetary stimulus package lowers the deposit facility rate to -0.5 % and restarts QE at a ...

» New ECB QE and its effects on interest rat...

The ECB is expected to introduce new unconventional monetary policy measures. First, we cal...