USA: The ‘Mid-cycle’ adjustment in key interest rates is done & Euro Area: Germany could be the weakest link (Martin Ertl)

US: The ‘Mid-cycle’ interest rate adjustment is done.

- The Fed concludes its adjustment in the key interest rate as the economy continues a solid expansion but some weak spots occur.

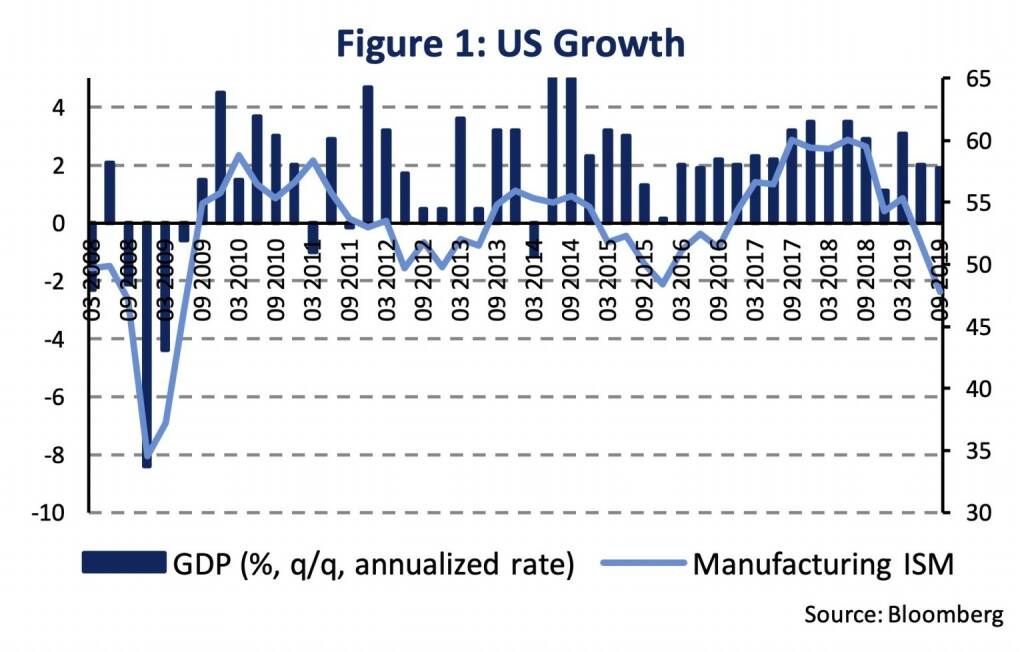

In Q3 2019 the US economy continued its expansion. Real gross domestic product (GDP) rose by 1.9 % (q/q, annualized rate) after 2.5 % during H1 2019. The expenditure components reveal that growth remains driven by personal consumption expenditure (2.9 %), while the second consecutive decline in fixed investment (-1.3 %) indicates weakening business dynamism. Investment in structures and equipment fell by 15.3 % and 3.8 % whereas residential investment rose by 5.1 %. In addition, net exports again deducted from GDP growth as imports growth outpaced exports (1.2 % and 0.7 %). Finally, government consumption contributes to GDP growth by rising 2.0 %. Hence, while a solid expansion of the US economy continued, the details show unbalanced growth relying mostly on household consumption.

In addition to the one-sided GDP growth, weak spots of the business cycle can be observed. Weak industry prospects – industrial production fell slightly in September (-0.1 % y/y) – were confirmed by the ISM manufacturing survey in October. The index keeps indicating a contraction in US manufacturing, though it stabilized (48.3 after 47.8). Furthermore, job growth has slowed steadily since the beginning of the year. In October, 128.000 new jobs were (non-farm payrolls) created after 180.000 in the preceding month. The jobs figure was better than expected but is in line with weaker business momentum.

On Wednesday, the Federal Open Market Committee (FOMC) lowered the target range of the federal funds rate by 25 basis points to 1.50-1.75 %. It was the last move of a ‘mid-cycle’ adjustment consisting of three reductions of the federal funds rate. In its statement, the FOMC referred to “implications from global developments for the economic outlook as well as muted inflations pressures” to justify the adjustment. President Powell referred to weakness in global growth and trade developments and said that the action provides “some insurance against ongoing risks”. The action supports the sustained expansion, the strong labor market and inflation near the 2 % objective but, at the same time, the FOMC stresses that uncertainties about this outlook remain. After the well communicated mid-cycle move, the FOMC will monitor incoming information to assess the appropriate path of the federal funds rate (‘data dependence’).

The Q3 GDP growth outcome was in line with the Fed’s projection for 2019 growth (2.2 %). The Atlanta and NY Fed’s nowcasting models currently signal 1.1 % and 0.8 % (q/q, annualized) GDP growth for the final quarter of the year. These first growth signals point to a further cooling of the US economy.

Euro Area: Germany could be the weakest link

- Weak growth but no negative surprises in Q3

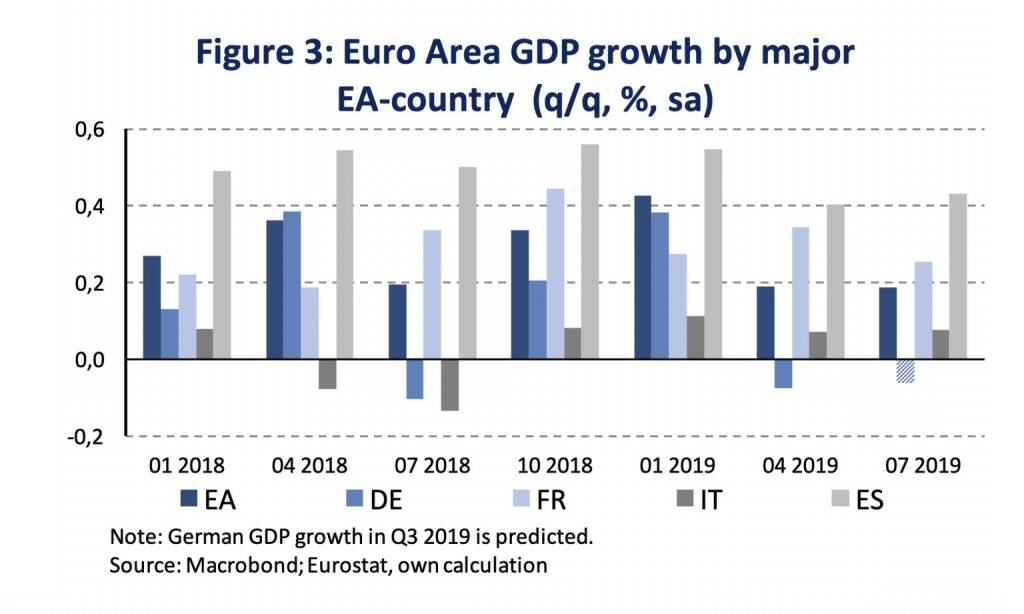

According to the first release, the Euro Area real GDP rose by 0.2 % (q/q) in Q3 after 0.3 % during H1 2019. In annual terms, GDP enhanced by 1.2 % in Q3 after 1.9 % during the total of 2018. The outcome came as a surprise to us as our nowcasting model signaled zero growth, hence, it must be watched how revisions come out.

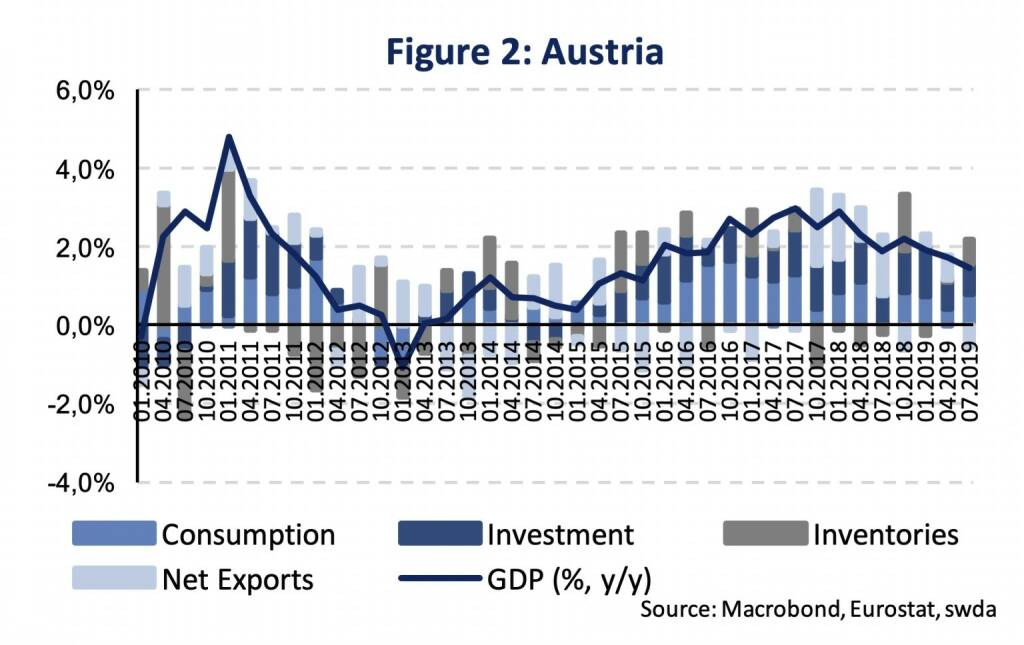

The cooling of the Austrian economy continued. Austria’s GDP growth was 0.2 % (q/q, Wifo trend-business cycle) and 1.5 % annually (Figure 2).

The outcome was again anticipated by our nowcasting model. GDP rose by just 0.1 % (q/q) in Q3 according to the Eurostat calculation (Figure 2). Household consumption expenditure remains solid, while the industrial sector is in a clear slowdown.

Among other Euro countries, GDP kept expanding in Spain (0.4 % q/q), France (0.3 %), Belgium (0.4 %) and Italy (0.1 %). German GDP will be released on 14th November. If we back out Germany’s growth from total Eurozone and available country-level data, our estimate for German Q3 growth is -0.1 % (Figure 3). Hence, while overall cross-country growth contained no negative surprises, Germany could encounter a GDP decline for the second consecutive quarter.

Authors

Martin Ertl Franz Xaver Zobl

Chief Economist Economist

UNIQA Capital Markets GmbH UNIQA Capital Markets GmbH

Latest Blogs

» SportWoche Podcast #124: Liam Ferguson, de...

» Österreich-Depots: Ultimo-Bilanz mit Addik...

» Börsegeschichte 30.8.: Warren Buffett (Bör...

» PIR-News: Zahlen von Warimpex, Strabag, Ne...

» Nachlese: Karin Bauer, LLB Aktien Österrei...

» Wiener Börse Party #727: Nächster Rekord-T...

» Börsenradio Live-Blick 30/8: DAX krönt Erh...

» Börse-Inputs auf Spotify zu u.a. ATX TR, L...

» ATX-Trends: Immofinanz, UBM, CA Immo, S Im...

» Börsepeople im Podcast S14/17: Karin Bauer

Weitere Blogs von Martin Ertl

» Stabilization at a moderate pace (Martin E...

Business and sentiment indicators have stabilized at low levels, a turning point has not yet b...

» USA: The ‘Mid-cycle’ adjustment in key int...

US: The ‘Mid-cycle’ interest rate adjustment is done. The Fed concludes its adj...

» Quarterly Macroeconomic Outlook: Lower gro...

Global economic prospects further weakened as trade disputes remain unsolved. Deceleration has...

» Macroeconomic effects of unconventional mo...

New monetary stimulus package lowers the deposit facility rate to -0.5 % and restarts QE at a ...

» New ECB QE and its effects on interest rat...

The ECB is expected to introduce new unconventional monetary policy measures. First, we cal...