Central banks’s forecast adjustments (Martin Ertl)

USA

- Fed FOMC increases the federal fund rate for the third time this year

- Federal fund rate target range at 1.25-1.5 %

- December economic projections show stronger labor market and higher GDP growth

In line with market expectations, the Federal Open Market Committee (FOMC) has decided to increase the target range of the federal funds rate by 25 basis points (bp) to 1.25-1.5 % from previously 1-1.25 %. This is the third rate hike this year after a 25 bp increase in March as well as June. The FOMC expects “economic conditions to evolve in a manner that will warrant gradual increases in the federal funds rate”. The statement also emphasises that the key policy rate is likely to remain below its longer run level “for some time”.

According to the December economic projections of the Federal Reserve Board and the FOMC, the median projection of the longer run federal funds rate is 2.8 %. The term longer-run refers to “five or six years” and reflects the federal fund rate which is compatible with the economy’s normal or trend rate of growth and its natural unemployment rate over the longer run. Hence, in the absence of further shocks the federal fund rate is expected to double over the longer run.

The Federal Reserve follows a dual mandate of maximum employment and price stability. Inflation is expected to remain below the Committee’s 2 % objective in the near term but stabilize around 2 % over the medium term. In October, the Personal Consumption Expenditure (PCE) Inflation was 1.6 % and Core PCE Inflation 1.4 %. The December economic projections expect PCE inflation to fulfil the 2 % objective in 2019. The expected path of inflation has remained unchanged compared to the September projections, except for a 0.1 %-point higher PCE inflation in 2017. The FOMC interprets the surprising softness of inflation seen in 2017 as transitory, yet admitting that their understanding of the forces driving inflation is imperfect.

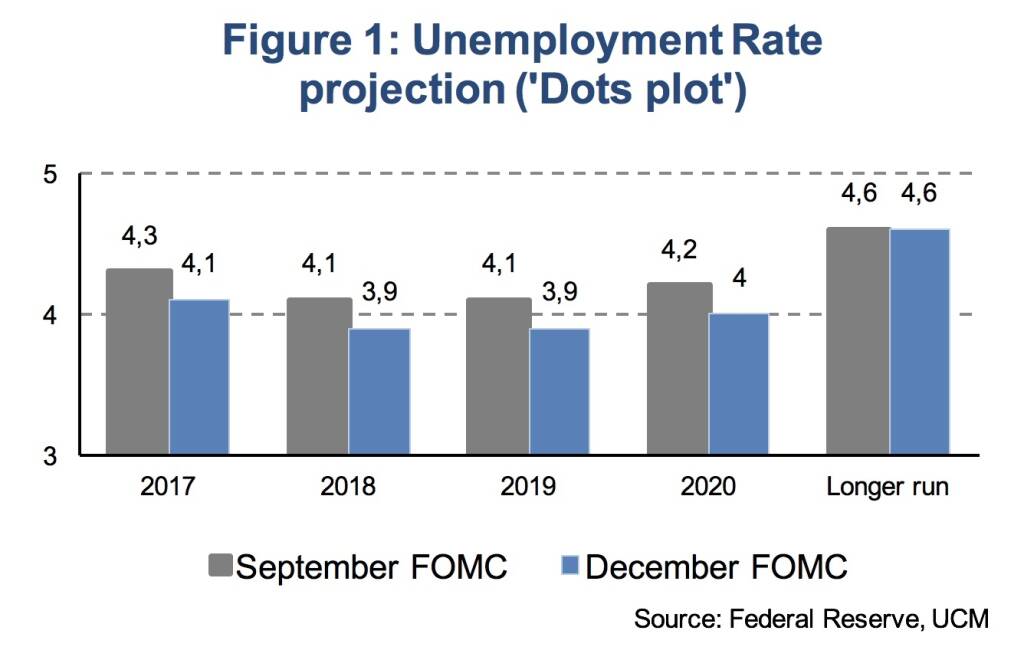

With respect to the Fed’s second objective, maximum employment, the FOMC expects “economic activity [to] expand at a moderate pace and labor market conditions [to] remain strong”. Compared to last month’s statement the FOMC changed its wording from “labor market conditions will strengthen somewhat further” to “labor market conditions will remain strong”. In October, the unemployment rate has decreased to 4.1 %, which is the lowest level since December 2000. It remained at 4.1 % in November. The December economic projections indicate that the labor market strengthened faster than the FOMC expected. Projected unemployment was lowered by 0.2 %-points over the whole projection period, from 2017 to 2020. For the years 2018 and 2019 the FOMC expects the unemployment rate to be 3.9 %. This is well below the longer run, normal, unemployment rate of 4.6 % (Figure 1).

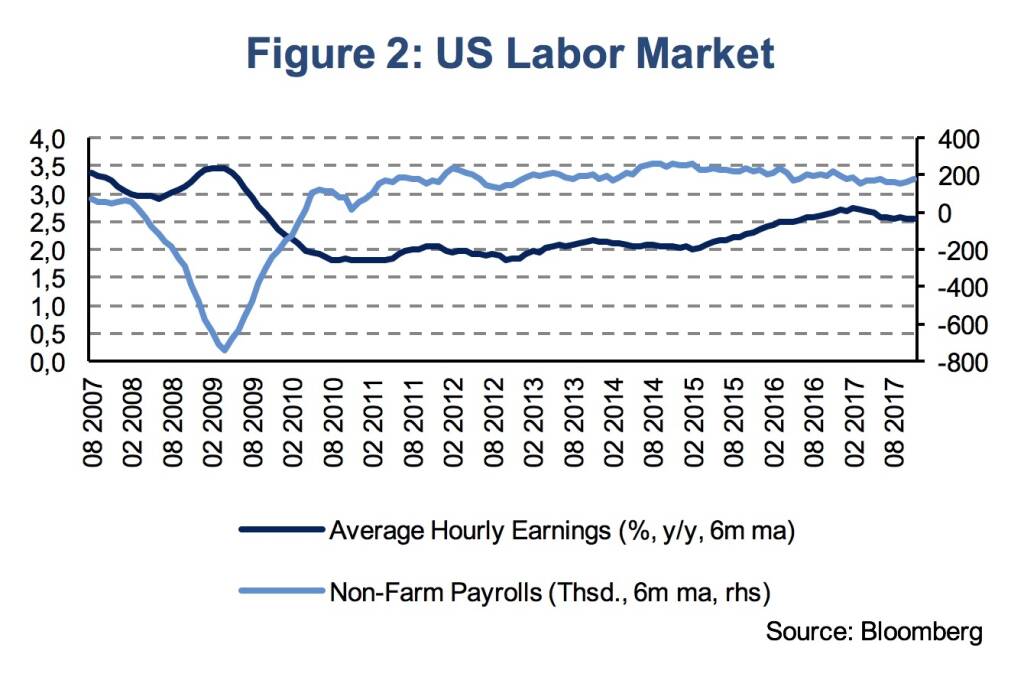

In the FOMC press conference, Janet Yellen, the Chair of the Committee, points out that “allowing the labor market to overheat would raise the risk that monetary policy would need to tighten abruptly at a later stage jeopardize the economic expansion”. Moderate wage growth indicates that the labor market is not overheated, yet, the US has reached full employment. (Figure 2)

In addition to the downward adjustment of the projections of the unemployment rate, the projection of real GDP growth was revised upwards. The most significant change has been made for the year 2018, with growth now being projected at 2.5 %, which is 0.4 %-points higher compared to the September projection. This is mainly, but not solely, due to anticipated growth effects of the planned tax reform (Tax Cuts and Jobs Act). There is large uncertainty with respect to its growth stimulus ranging from below 0.1 %-points per annum over a ten-year period from the Joint Committee on Taxation (JCT) to 0.7 %-points per annum from the Treasury’s Office of Tax Policy (OTP). Hence, President Trump’s tax reform remains a source of economic uncertainty despite the very near-term passing of the bill at Congress.

Eurozone

- ECB monetary policy stance was unchanged in December, as expected.

- Long-term confidence to reach the inflation target is mitigated by short-term inflation soft patch.

At the meeting of the governing council (GC) that took place last Thursday, the European Central Bank left the main policy interest rates unchanged. The pivotal forward-looking message that the GC “expects the key policy rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases”, was also left unchanged. Regarding the unconventional monetary policy instruments, the GC confirmed that from January 2018 it intends to continue to make net asset purchases under the asset purchase programme (APP) at a monthly pace of 30 bn EUR until September 2018. If necessary, the APP will extend beyond this date, in case the GC does not see a sustained adjustment in the path of inflation toward the ECB’s inflation goal. The ECB will also continue to reinvest principal payments from maturing securities for an extend period of time after the end of the net asset purchases.

With respect to the economic outlook, the ECB sees a strong pace of economic expansion and a significant improvement in the outlook. The significant reduction in economic slack gives ground for greater confidence that inflation will converge towards the inflation goal, according to President Draghi’s introductory remarks at last Thursday’s press conference. At the same time, price pressures remain muted overall and an “ample degree of monetary stimulus remains necessary”.

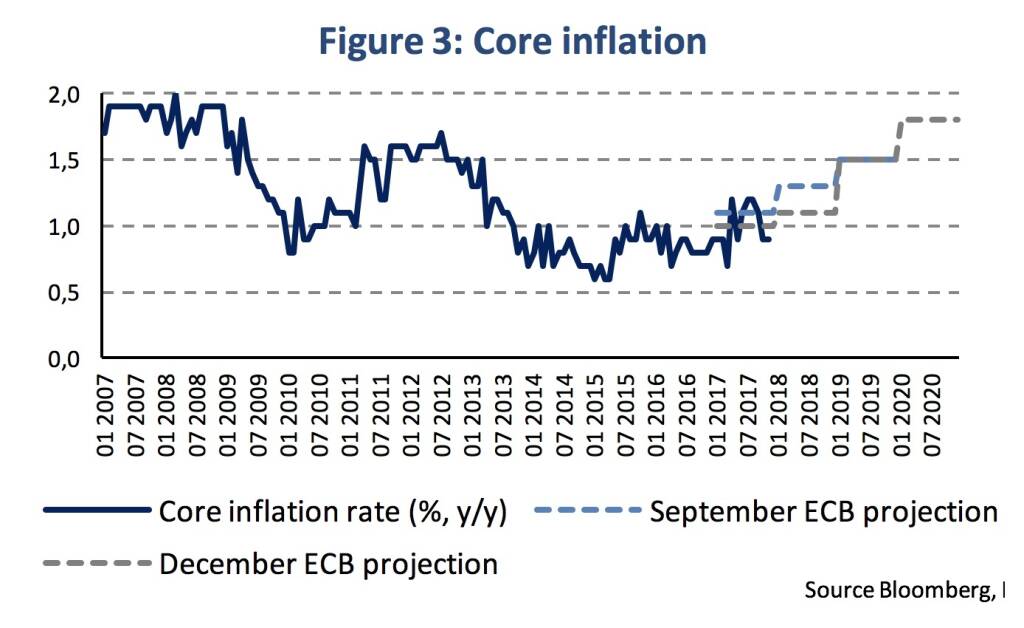

Based on the updated staff macroeconomic projections as of December, Euro Area real GDP is foreseen to expand by 2.3 %, 1.9 % and 1.7 % from 2018 to 2020. Compared to the September outlook (1.8 % and 1.7 % in 2018-19), growth has been upgraded significantly. The inflation rate is projected to at 1.4 %, 1.5 % and 1.7 % between 2018 and 2020. For 2018, the inflation forecast has been revised up (from 1.2 % previously) mainly due to higher oil and food prices. The oil price assumption for 2018 has increased from 52.6 in the September outlook to 61.6 USD/bl in the updated forecast. However, the core inflation projection for next year was decreased to 1.1 % from 1.3 % previously, while it is expected to rise to 1.5 % in 2019 and 1.8 % in 2020. Hence, this reflects confidence to reach its inflation goal in the longer run, while the core consumer price trends remain muted and almost unchanged to 2017 (core inflation on average of 1.0 %) during the next year (Figure 3). The discrepancy between significant improvements in the growth outlook and subdued fundamental price trends remains the main policy dilemma for the ECB.

Authors

Martin Ertl Franz Zobl

Chief Economist Economist

UNIQA Capital Markets GmbH UNIQA Capital Markets GmbH

Disclaimer

This publication is neither a marketing document nor a financial analysis. It merely contains information on general economic data. Despite thorough research and the use of reliable data sources, we cannot be held responsible for the completeness, correctness, currentness or accuracy of the data provided in this publication.

Our analyses are based on public Information, which we consider to be reliable. However, we cannot provide a guarantee that the information is complete or accurate. We reserve the right to change our stated opinion at any time and without prior notice. The provided information in the present publication is not to be understood or used as a recommendation to purchase or sell a financial instrument or alternatively as an invitation to propose an offer. This publication should only be used for information purposes. It cannot replace a bespoke advisory service to an investor based on his / her individual circumstances such as risk appetite, knowledge and experience with financial instruments, investment targets and financial status. The present publication contains short-term market forecasts. Past performance is not a reliable indication for future performance.

Latest Blogs

» SportWoche Podcast #155: Lili Tagger und A...

» Börse-Inputs auf Spotify zu u.a. Ex-Börseh...

» Österreich-Depots: Irre Weekend Bilanz, ab...

» Börsegeschichte 4.4.: Das wird wohl einer ...

» Nachlese: Danke Sophie Wotschke, Rudi Grei...

» Wiener Börse Party #877: Grösster ATX TR-P...

» PIR-News: Pierer Mobility, AMAG, BKS Bank,...

» 618 intraday vs. 605 (Christian Drastil)

» Börse-Inputs auf Spotify zu u.a. gettex-Po...

» Börsepeople im Podcast S18/08: Max Pohanka

Weitere Blogs von Martin Ertl

» Stabilization at a moderate pace (Martin E...

Business and sentiment indicators have stabilized at low levels, a turning point has not yet b...

» USA: The ‘Mid-cycle’ adjustment in key int...

US: The ‘Mid-cycle’ interest rate adjustment is done. The Fed concludes its adj...

» Quarterly Macroeconomic Outlook: Lower gro...

Global economic prospects further weakened as trade disputes remain unsolved. Deceleration has...

» Macroeconomic effects of unconventional mo...

New monetary stimulus package lowers the deposit facility rate to -0.5 % and restarts QE at a ...

» New ECB QE and its effects on interest rat...

The ECB is expected to introduce new unconventional monetary policy measures. First, we cal...