The divergence of two central banks: Fed and ECB outline paths of monetary policy normalization (Martin Ertl)

- The Federal Reserve Bank (Fed) increases key interest rates and signals a faster rate hiking cycle.

- The European Central Bank (ECB) adjusts its forward guidance on interest rates expecting rates to remain at their present levels at least through the summer of 2019.

- The ECB’s net asset purchases (QE) will end this year after a reduction of net asset purchases to 15 billion EUR per month from October onwards.

- The Euro Area continues to show lower potential growth and an unemployment rate still above the natural rate of unemployment.

Last week was dominated by long-awaited central bank decisions on monetary policy normalization. The members of the Federal Open Market Committee (FOMC) of the Federal Reserve Bank (Fed) met on June 12-13 to discuss the stance of monetary policy consistent with recent positive signals from the US economy. It was decided to raise the target range of the federal funds rate by 25 basis points to 1.75 - 2 % reflecting a “sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 % objective over the medium term”. On Thursday, the Euro Area’s central bankers met in Riga, Latvia, to discuss “whether progress so far has been sufficient to warrant a gradual unwinding of […] net asset purchases”, also known as quantitative easing (QE) [1]. And indeed, the Governing Council anticipates stopping net asset purchases by the end of 2018 after a reduction of net purchases to 15 billion EUR per month in October. Additionally, “the Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019”.

Once again, the ECB’s president, Mario Draghi, emphasized the importance of patience, prudence and consistency. The Governing Council has gained confidence in the sustained convergence of inflation towards the ECB’s objective, yet underlying inflation remains generally muted. Hence, Mario Draghi was eager to emphasize certain elements of optionality. The path of monetary policy normalization, which has been presented, is conditional on “incoming data confirming the Governing Council’s medium-term inflation outlook”. That’s the case for the gradual winding-down of the net asset purchases until the end of the year, as well as the suggested time dimension given to the first increase in key interest rates. With respect to the latter the ECB’s president reiterated that “key ECB interest rates remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path”. To sum up, the ECB anticipates stopping its balance sheet expansion by the end of the year but intends to reinvest principal payments from maturing securities for an extended period of time. Additionally, the forward guidance on interest rates has been altered by signaling the first rate hike not to occur before Q3 2019. Thus, last week’s ECB meeting has presented some long-awaited guidance on the ECB’s path of monetary policy normalization but, at the same time, has signaled that the path will be adjusted if incoming data question the sustained adjustment path of inflation.

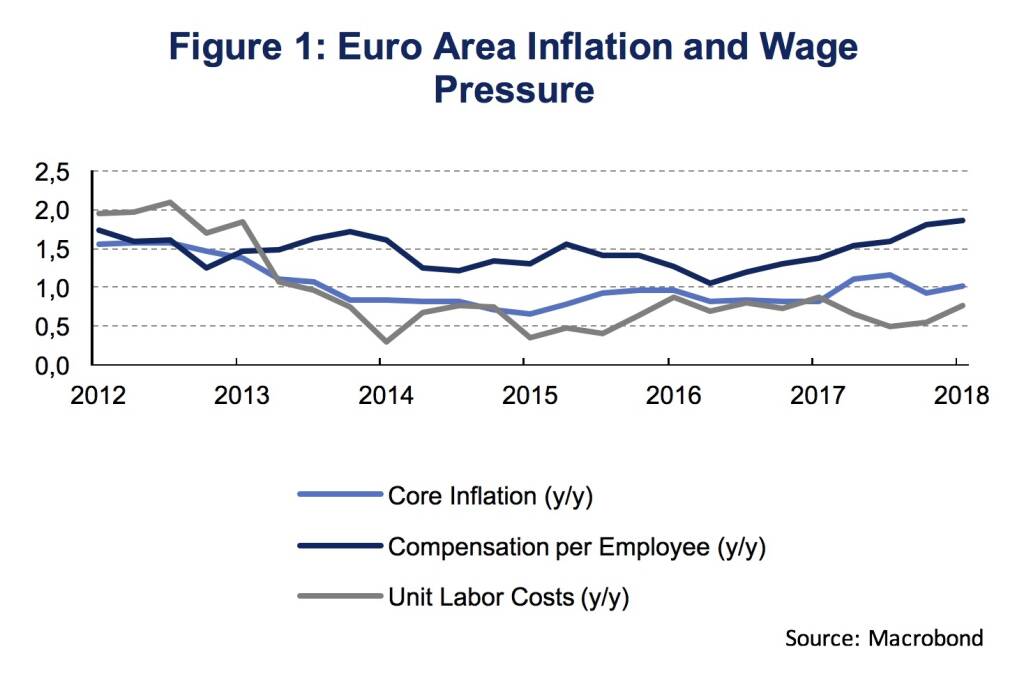

Euro Area inflation has lately surged mainly due to higher energy prices. Harmonized Consumer Price Inflation was at 1.9 % in May 2018 to which energy prices contributed 0.6 %-age points. Core inflation, which excludes energy and food prices from the HICP Index, is markedly lower. In May 2018 core inflation was at 1.1 % while the three months moving average is 1.0 %. These recent developments have translated into revisions of the Eurosystem staff macroeconomic projections. In line with our assessment, as discussed in last week’s UNIQA Capital Markets Weekly, the 2018 projection for headline HICP inflation has been increased while the 2018 projection for core inflation has remained unchanged. Headline HICP inflation is now projected at 1.7 % for 2017, up by 0.3 %-age points compared to the March projection, while the 2018 projection of core inflation has been kept constant at 1.1 %. In spite of only moderate advances in core inflation, the ECB “concluded that progress towards a sustained adjustment in inflation has been substantial so far”. One reasons for this assessment was that wage growth has accelerated. The growth rate of compensation per employees, the wage series which Mario Draghi has mentioned during the press conference, has increased to 1.9 % (y/y) in Q1 2018. Figure 1 shows the marked increase in trend growth of compensation per employee since 2016. At the same time, however, unit labor cost growth, which additionally accounts for changes in labor productivity, stayed rather flat. Needless to say, that higher productivity growth is a positive sign for the Euro Area economy, it also highlights that wage growth might need to accelerate even further in order to stimulate a sustained adjustment in core inflation.

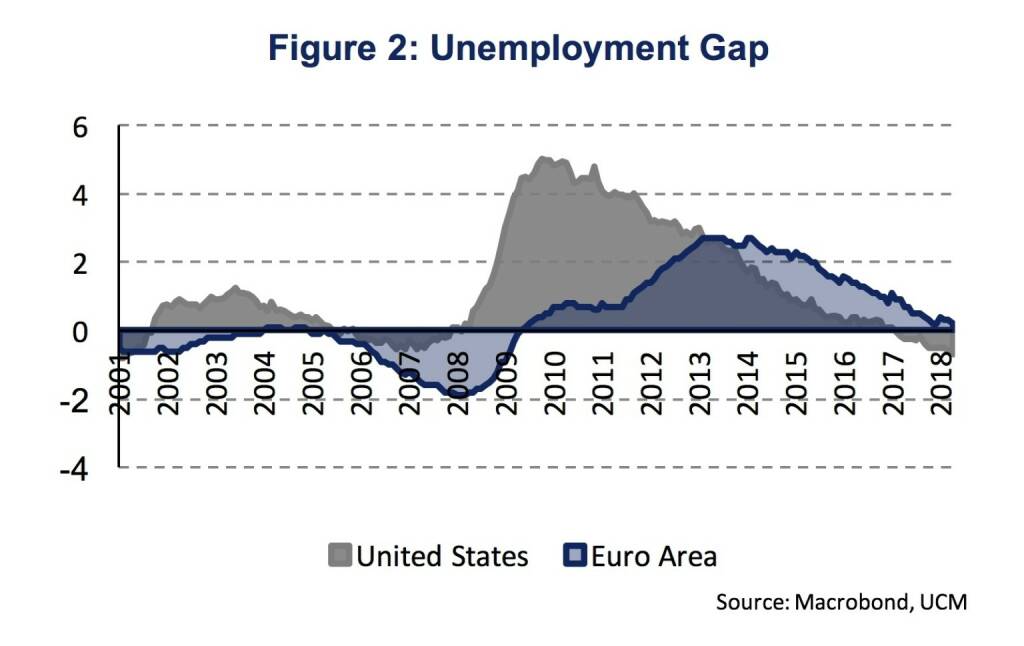

One reason why Mario Draghi was more cautious in signaling tighter monetary policy compared to Jerome Powell, the FOMC’s Chairman, is the still elevated level of unemployment in the Euro Area. The unemployment rate in the United States has reached 3.8 % in May, while the unemployment rate in the Euro Area was 8.5 % in April. From a monetary policy perspective looking at the unemployment rate in isolation is less informative. The unemployment rate needs to be set in relation to the natural rate of unemployment (NAIRU), in order to gauge whether the labor market is tight and creates inflationary pressure. Figure 2 shows the unemployment gap, which is the difference between the NAIRU and the unemployment rate, for the United States and the Euro Area. The most important take-away from figure 2 is that the unemployment gap is still positive in the Euro Area, while it turned negative in the United States in early 2017. Based on the latest ECB staff macroeconomic projections (June 2018), the Euro Area’s unemployment rate will fall below the natural rate of unemployment in 2019, with the unemployment rate at 7.8 % and the NAIRU at 8.1 % [2]. The natural rate of unemployment is not static and has also been decreasing, however, less rapidly than the unemployment rate. For the United States the natural rate of unemployment is estimated to have decreased from 5.1 % in 2011 to 4.6 % in 2015 since when it has remained constant (CBO). As Jerome Powell has noted in the press conference following the June FOMC meeting, “we have to acknowledge that there are always wide uncertainty bands around the level of, for example, the natural rate of unemployment”. Hence, in addition to concepts like the natural rate of unemployment, or the natural rate of interest, incoming data are important to guide the FOMC’s assessment whether monetary policy is accommodative, neutral, or restrictive. This is well in line with Mario Draghi’s emphasis on optionality.

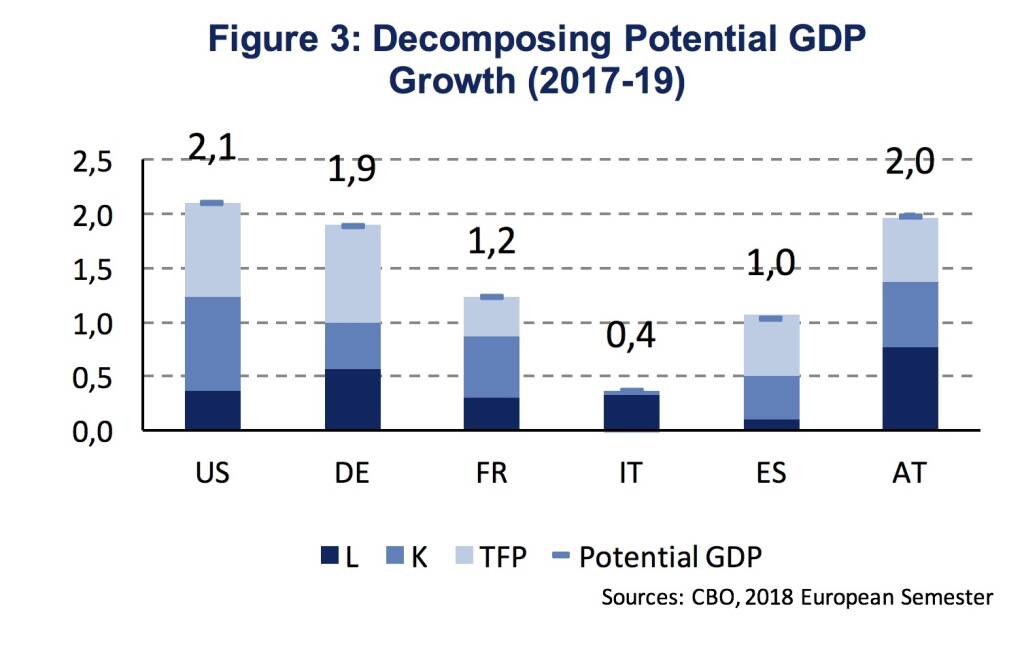

Based on the comparison of unemployment gaps, the US labor market is tighter than in the Euro Area which justifies a faster pace of monetary policy normalization in the United States. In addition to this medium-term assessment, also the short-term economic growth momentum seems to be more dynamic in the United States. This is well reflected in the updated macroeconomic projections of both central banks. While the GDP growth projection for 2018 was revised upwards to 2.8 % (+0.1 %-age points) for the US economy, the projection was revised downwards to 2.1 % (-0.3 %-age points) for the Euro Area economy. Despite the growth moderation in the Euro Area, the downward adjusted 2018 growth projection remains well above the Euro Area’s potential growth rate of around 1.5 %. Potential growth is higher in the United States at around 2 % [3]. Figure 3 shows a decomposition of potential GDP growth for the United States, the four largest Euro Area economies and Austria based on an average of 2017 to 2019. Potential growth varies quite substantially across Euro Area economies. While potential growth is close to the US level in Germany and Austria, it is substantially lower in France and Spain. Italy shows the lowest potential growth rate of GDP across the whole sample at 0.4 %. Looking at the sources of potential growth shows that Italy lacks investment (growth of the capital stock K) and productivity growth (TFP). Productivity growth, which is the most sustainable long-term growth driver, is also muted in France, while Spain has managed to boost productivity growth above pre-crisis levels. The high level of structural unemployment, however, weighs on the country’s growth potential, with a slow growth of labor supply (L). To conclude, the Euro Area needs to boost potential growth by increasing labor supply (reducing structural unemployment, increasing labor force participation rates or im-/migration), stimulate investment and productivity growth.

[1]The intention to discuss the future pace of the ECB’s QE program has been express by Peter Praet, a member of the executive board of the ECB.

[2]The Euro Area’s natural rate of unemployment is derived from the Macro-economic database AMECO, which is the annual macro-economic database of the European Commission’s Directorate General for Economic and Financial Affairs. For the United States the natural rate of unemployment has been derived from the U.S. Congressional Budget Office (CBO).

[3]Estimates of potential growth in 2018 for the United States lie between 1.6 % (OECD) and 2.3 % (AMECO). The CBO estimates potential growth at 1.9 %.

Authors

Martin Ertl Franz Zobl

Chief Economist Economist

UNIQA Capital Markets GmbH UNIQA Capital Markets GmbH

Latest Blogs

» BSN Spitout Wiener Börse: Mit Erste, Bawag...

» SportWoche Party 2024 in the Making, 23. A...

» SportWoche Party 2024 in the Making, 25. A...

» Österreich-Depots: Unverändert (Depot Komm...

» Börsegeschichte 25.4.: RBI, Porr (Börse Ge...

» Zahlen von Strabag, News von Marinomed, S ...

» Wiener Börse Party #637: Egalite Addiko Ba...

» Nachlese: Marcel Hirscher, Hannes Roither,...

» Wiener Börse zu Mittag schwächer: Frequent...

» MMM Matejkas Market Memos #35: Gedanken üb...

Weitere Blogs von Martin Ertl

» Stabilization at a moderate pace (Martin E...

Business and sentiment indicators have stabilized at low levels, a turning point has not yet b...

» USA: The ‘Mid-cycle’ adjustment in key int...

US: The ‘Mid-cycle’ interest rate adjustment is done. The Fed concludes its adj...

» Quarterly Macroeconomic Outlook: Lower gro...

Global economic prospects further weakened as trade disputes remain unsolved. Deceleration has...

» Macroeconomic effects of unconventional mo...

New monetary stimulus package lowers the deposit facility rate to -0.5 % and restarts QE at a ...

» New ECB QE and its effects on interest rat...

The ECB is expected to introduce new unconventional monetary policy measures. First, we cal...